Economic Thought – Origin of Economic Ideas in a Historical Context

Economic thought has evolved over time as economists have tried to explain how economies function and how problems such as scarcity, growth, and inequality can be addressed. Each period reflects the economic conditions and challenges of its time.

Economic thought = Evolution of ideas to explain and improve economies

Key Ideas:

- Economic theories develop in response to real-world problems.

- Different schools of thought offer different solutions.

- Modern economics builds on ideas from earlier periods.

- Understanding history helps in evaluating current policies.

18th Century: Adam Smith and Laissez Faire

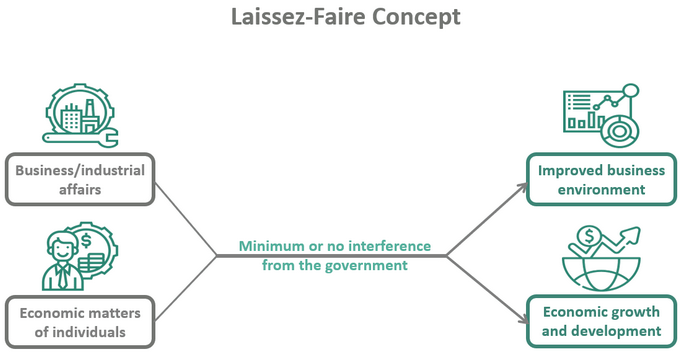

The 18th century marks the origin of modern economic thought with the work of Adam Smith. He argued that economies function efficiently when individuals are free to make their own economic decisions with minimal government intervention.

Laissez faire refers to a system where markets operate freely without significant government control. Economic decisions are guided by the interaction of demand and supply.

Core Ideas:

- Self-interest drives economic decisions by consumers and firms.

- The invisible hand explains how individual actions lead to efficient outcomes for society.

- Price mechanism allocates resources through demand and supply.

- Competition promotes efficiency and innovation.

- Government role is limited to basic functions such as law and order.

Implications:

- Markets determine what, how, and for whom to produce.

- Resources are allocated based on consumer preferences.

- Encourages efficiency and economic growth.

Evaluation Insight:

- Effective in promoting efficiency in competitive markets.

- May fail in cases of market failure such as inequality or externalities.

- Modern economies use a mixed approach rather than pure laissez faire.

Example

Explain how the price mechanism allocates resources in a laissez faire economy.

▶️ Answer / Explanation

In a laissez faire economy, prices are determined by demand and supply.

If demand for a product increases, its price rises, signaling firms to produce more.

Resources are then allocated to the production of that good.

This ensures that goods are produced according to consumer preferences without government intervention.

19th Century: Classical Economics and Marxist Critique

In the 19th century, economic thought developed further through classical economics, which focused on how markets determine prices, output, and income distribution. Economists emphasized the role of individuals and firms in making decisions based on incentives.

Core Ideas of Classical Economics:

- Utility explains how consumers gain satisfaction from goods and services.

- Marginal analysis focuses on decision-making at the next unit, such as marginal cost and marginal benefit.

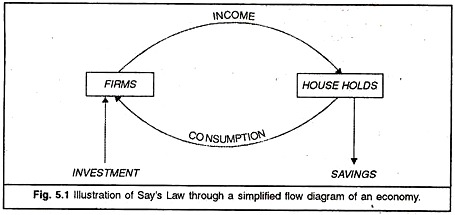

- Say’s Law states that supply creates its own demand, implying markets tend toward full employment.

- Markets are generally self-regulating with minimal need for intervention.

Marxist Critique:

At the same time, Karl Marx criticized classical economics, focusing on inequality within capitalist systems.

- Capitalism leads to unequal distribution of income and wealth.

- Workers may be exploited, receiving less than the value they produce.

- Economic systems are shaped by class conflict between workers and owners.

- Advocated alternative systems with greater equality.

Implications:

- Decisions are based on marginal thinking by consumers and firms.

- Markets are assumed to achieve equilibrium and full employment.

- Highlights both efficiency of markets and concerns about inequality.

Evaluation Insight:

- Marginal analysis remains a key tool in modern economics.

- Say’s Law may not hold during periods of low demand or recession.

- Marxist ideas highlight inequality but may overlook benefits of market efficiency.

- Modern economics considers both efficiency and equity.

Example

Explain the importance of marginal analysis in economic decision-making.

▶️ Answer / Explanation

Marginal analysis involves making decisions based on additional costs and benefits.

For example, a firm will produce more units of a good as long as the marginal revenue exceeds the marginal cost.

This helps firms maximize profit and allocate resources efficiently.

Thus, marginal thinking is essential for rational economic decision-making.

20th Century: Keynesian Revolution and Monetarist/New Classical Counter-Revolution

The 20th century saw major changes in economic thought, especially due to events like the Great Depression. These events challenged earlier ideas and led to new approaches focusing on managing the overall economy.

Keynesian Revolution:

- John Maynard Keynes argued that economies may not always achieve full employment.

- Low aggregate demand can lead to unemployment and recession.

- Government should use fiscal policy such as spending and taxation to stabilize the economy.

- Emphasis on active government intervention.

Monetarist and New Classical Counter-Revolution:

- Focused on the role of money supply in controlling inflation.

- Argued that markets tend to be self-correcting in the long run.

- Believed excessive government intervention can cause instability.

- Supported rules-based policies rather than discretionary actions.

Implications:

- Development of macroeconomic policy to manage economic fluctuations.

- Recognition that governments play an important role in stabilizing economies.

- Ongoing debate between intervention and free market approaches.

Evaluation Insight:

- Keynesian policies are effective during economic downturns.

- Monetarist approaches are useful in controlling inflation.

- Modern economies combine both approaches.

- Balance between intervention and market forces is essential.

Example

Explain why Keynesian economics supports government intervention.

▶️ Answer / Explanation

Keynesian economics argues that low aggregate demand can lead to unemployment and recession.

In such situations, markets may not automatically correct themselves.

Therefore, the government can increase spending or reduce taxes to boost demand.

This helps increase production, employment, and economic activity.

21st Century: Behavioural Economics, Interdependence, and Sustainability

In the 21st century, economic thought has expanded beyond traditional models to include insights from other disciplines and to address global challenges. There is greater recognition that economies are influenced by human behaviour, global interdependence, and environmental limits.

Behavioural Economics:

- Challenges the assumption that individuals are always rational decision-makers.

- Incorporates insights from psychology to explain behaviour.

- Decisions are influenced by biases, habits, and emotions.

- Policies may use nudges to guide better choices.

Interdependence and Globalization:

- Economies are increasingly connected through trade, finance, and technology.

- Actions in one country can affect others.

- Highlights the importance of global cooperation.

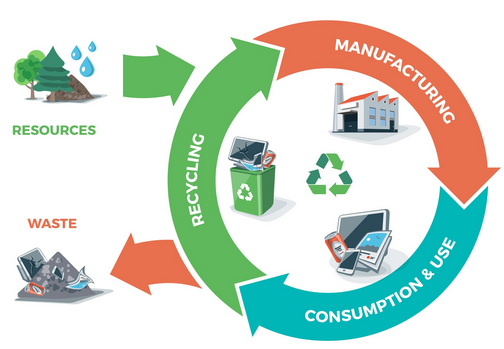

Sustainability and Circular Economy:

- Focus on meeting present needs without harming future generations.

- Recognizes limits of natural resources and environmental impact.

- The circular economy promotes reuse, recycling, and reduced waste.

- Balances economic growth with environmental protection.

Modern economics = Behaviour + Global interdependence + Sustainability

Implications:

- Policies are designed considering real human behaviour.

- Greater focus on long-term sustainability.

- Economic decisions consider social and environmental impacts.

Evaluation Insight:

- Behavioural economics makes models more realistic.

- Sustainability is essential for long-term economic stability.

- Global interdependence increases both opportunities and risks.

- Balancing growth, equity, and sustainability remains a key challenge.

Example

Explain how behavioural economics differs from traditional economic theory.

▶️ Answer / Explanation

Traditional economic theory assumes that individuals are rational and make decisions to maximize utility.

Behavioural economics argues that decisions are influenced by psychological factors such as biases and habits.

For example, individuals may overspend due to impulse buying rather than rational planning.

This shows that behaviour is not always rational, making behavioural economics more realistic.