Economics as a Social Science – The Social Nature of Economics

Economics is a social science because it studies how individuals, firms, and governments make decisions about the allocation of scarce resources within a society. It focuses on human behaviour and interactions, rather than fixed natural laws.

The social nature of economics means that economic decisions are not made in isolation — they are influenced by relationships, institutions, culture, and societal structures. The choices made by one group affect others, creating a system of interdependence.

This includes:

- Interaction — Economic agents (consumers, firms, governments) interact in markets.

- Interdependence — Decisions by one group influence others.

- Social influence — Culture, norms, and values shape economic behaviour.

- Collective outcomes — Individual decisions combine to determine overall economic results.

Economics = Study of human behaviour + social interactions under scarcity

Key Ideas:

- Economic decisions are influenced by social and institutional factors.

- There are no fixed laws — outcomes vary across societies and time.

- Economic actions often create spillover effects on others.

- Understanding economics requires analysing both individual and group behaviour.

Economics as a Social Science vs Natural Sciences:

| Aspect | Economics (Social Science) | Natural Sciences |

|---|---|---|

| Focus | Human behaviour and decision-making | Physical laws and natural phenomena |

| Nature of Laws | General tendencies, not exact laws | Precise and universal laws |

| Predictability | Less predictable due to human behaviour | Highly predictable outcomes |

| Influence of Values | Strongly influenced by social and cultural factors | Independent of human values |

Types of Economic Interactions:

| Interaction | Description | Example |

|---|---|---|

| Consumer–Firm | Consumers purchase goods and services from firms. | Buying a laptop from a company. |

| Firm–Government | Firms follow regulations and pay taxes. | A business paying corporate tax. |

| Government–Consumer | Government provides public goods and services. | Public healthcare and education. |

| Global Interaction | Countries depend on each other through trade. | Importing raw materials from abroad. |

Example 1

Explain why economics is considered a social science.

▶️ Answer / Explanation

Economics is considered a social science because it studies how individuals and groups make decisions regarding the allocation of scarce resources. These decisions are influenced by social factors such as culture, values, and institutions.

Unlike natural sciences, economics does not deal with fixed laws. Human behaviour is unpredictable and varies across societies, making economic outcomes less certain.

Furthermore, economic decisions involve interaction between different agents such as consumers, firms, and governments. For example, a firm’s pricing decision affects consumers, while government policies influence both.

Therefore, economics focuses on human behaviour and social interactions, which is why it is classified as a social science.

Example 2

Using an example, explain how the social nature of economics leads to interdependence between economic agents.

▶️ Answer / Explanation

The social nature of economics means that economic agents are interconnected, and decisions made by one group affect others.

For example, an increase in fuel prices raises transportation costs for firms. As a result, firms increase the prices of goods and services. This affects consumers, who now have to pay higher prices.

At the same time, governments may intervene by reducing taxes or providing subsidies to control inflation, which further influences both firms and consumers.

This demonstrates interdependence, where the actions of one group create ripple effects throughout the economy due to the social nature of economic interactions.

The Basis of the Study of Economics: Microeconomics and Macroeconomics

Economics is broadly divided into two main branches: microeconomics and macroeconomics. These two areas provide different perspectives for analysing how an economy functions.

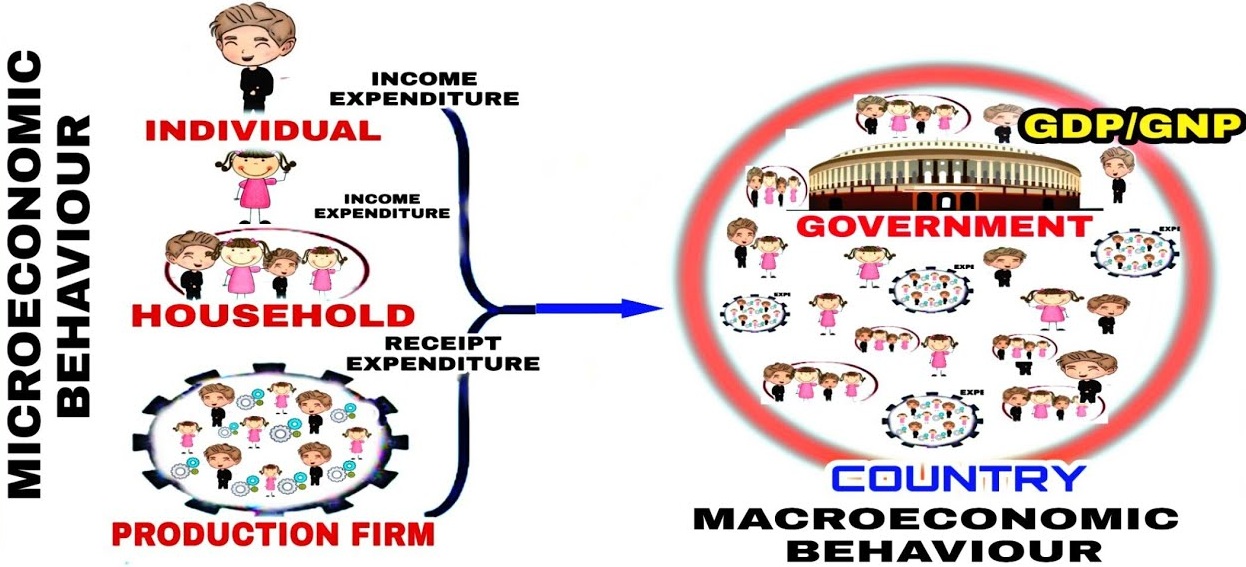

Microeconomics focuses on the behaviour of individual economic agents such as consumers, firms, and specific markets. It examines how decisions are made at a small (individual) level.

Macroeconomics studies the economy as a whole. It looks at large-scale economic variables such as national income, inflation, unemployment, and economic growth.

This division helps economists:

- Understand decision-making at both individual and aggregate levels.

- Analyse how small-scale interactions affect the overall economy.

- Develop policies to address both market-specific and economy-wide issues.

Economics = Microeconomics (individual units) + Macroeconomics (entire economy)

Key Ideas:

- Microeconomics deals with specific markets and decision-makers.

- Macroeconomics focuses on aggregate indicators of the economy.

- Both are interconnected — changes in one affect the other.

- Understanding both is essential for complete economic analysis.

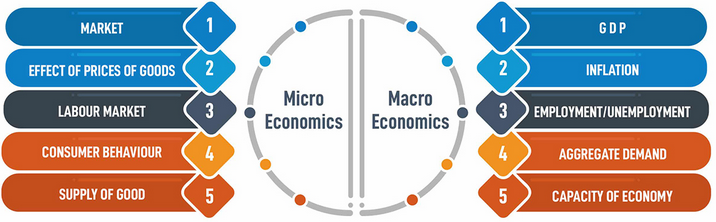

Comparison Between Microeconomics and Macroeconomics:

| Aspect | Microeconomics | Macroeconomics |

|---|---|---|

| Focus | Individual consumers, firms, and markets | Entire economy |

| Level of Analysis | Small-scale (individual units) | Large-scale (aggregate level) |

| Main Topics | Demand, supply, price determination | Inflation, unemployment, economic growth |

| Objective | Efficient allocation of resources | Stability and growth of the economy |

| Example | Price of a product in a market | Overall price level in the economy |

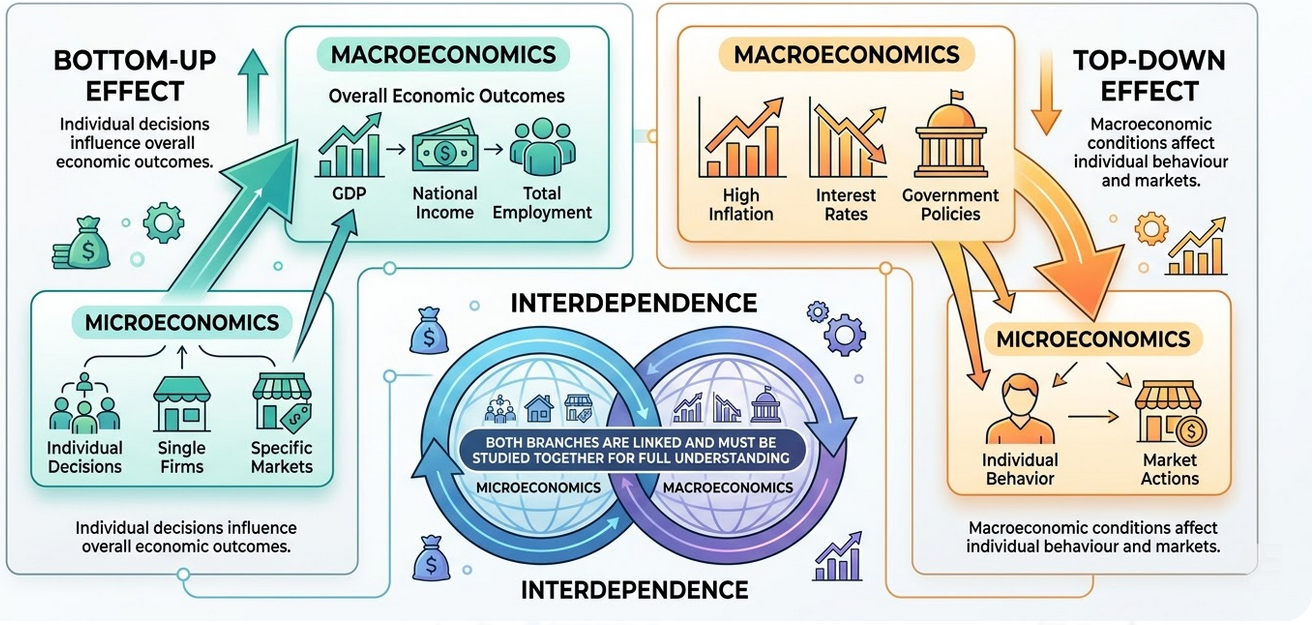

Relationship Between Microeconomics and Macroeconomics:

| Concept | Description |

|---|---|

| Bottom-up Effect | Individual decisions (micro) combine to influence overall economic outcomes (macro). |

| Top-down Effect | Macroeconomic conditions (e.g., inflation) affect individual behaviour and markets. |

| Interdependence | Both branches are linked and must be studied together for full understanding. |

Example 1

Explain the difference between microeconomics and macroeconomics.

▶️ Answer / Explanation

Microeconomics studies individual economic units such as consumers, firms, and specific markets. It focuses on how prices are determined and how resources are allocated at a small scale.

In contrast, macroeconomics studies the economy as a whole. It examines aggregate variables such as inflation, unemployment, and economic growth.

Thus, while microeconomics looks at individual decision-making, macroeconomics focuses on overall economic performance.

Example 2

Using an example, explain how microeconomic decisions can influence macroeconomic outcomes.

▶️ Answer / Explanation

Microeconomic decisions made by individuals and firms can collectively influence macroeconomic outcomes.

For example, if many consumers reduce their spending due to uncertainty, firms experience lower demand. As a result, firms may reduce production and lay off workers.

This leads to higher unemployment and slower economic growth at the macroeconomic level.

Therefore, individual (microeconomic) decisions can combine to affect the overall performance of the economy (macroeconomics).

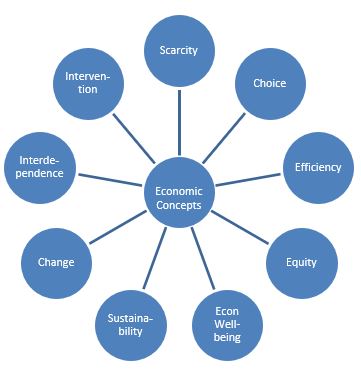

Introduction to the Nine Central Concepts

In DP Economics, understanding economic issues is supported by nine central concepts. These concepts act as tools to analyse real-world situations and help explain how economies function and evolve.

They are interconnected and often used together when evaluating economic problems and policies.

The nine central concepts are:

- Scarcity

- Choice

- Efficiency

- Equity

- Economic well-being

- Sustainability

- Change

- Interdependence

- Intervention

Central Concepts = Framework to analyse economic decisions and policies

Key Ideas:

- These concepts are used to structure economic thinking.

- Most real-world issues involve multiple concepts at once.

- They help in evaluation and essay writing in DP Economics.

- Understanding relationships between concepts is essential for higher-level answers.

Overview of the Nine Central Concepts:

The nine central concepts in DP Economics provide a structured framework to analyse economic decisions, policies, and real-world issues. Each concept is interconnected and is frequently applied in exam responses, especially in evaluation and real-world contexts.

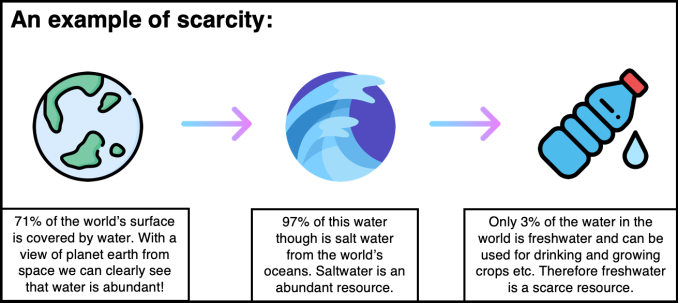

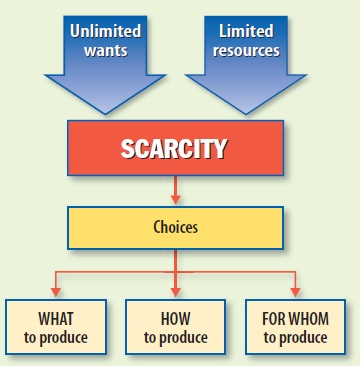

Scarcity

Scarcity refers to the fundamental economic problem that arises because resources are limited while human wants are unlimited. This forces individuals and societies to make decisions about how to allocate resources efficiently.

- Leads directly to choice and opportunity cost.

- Applies to all economies regardless of development level.

- Exists for both individuals (time, income) and governments (budgets).

- Forms the foundation of all economic analysis.

Choice

Choice is the decision-making process of selecting between alternatives due to scarcity. Every economic agent must decide how best to allocate limited resources.

- Every choice involves an opportunity cost.

- Applies to consumers (spending), firms (production), and governments (policy).

- Rational decision-making assumes maximizing benefit or utility.

- Key to understanding resource allocation.

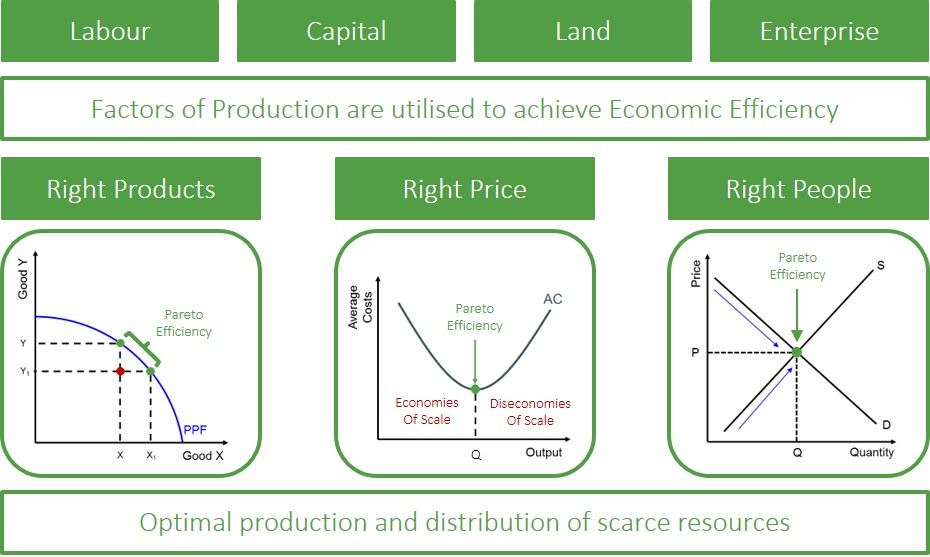

Efficiency

Efficiency refers to the optimal use of resources to maximize output and minimize waste. It ensures that society gets the most benefit from available resources.

- Includes allocative efficiency (resources match consumer preferences).

- Includes productive efficiency (lowest cost production).

- Dynamic efficiency focuses on innovation and future growth.

- Often evaluated in market structures and policy decisions.

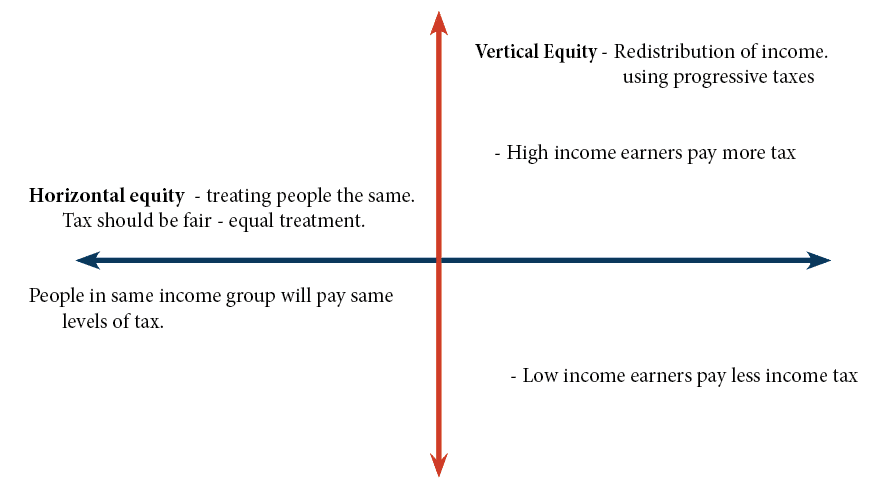

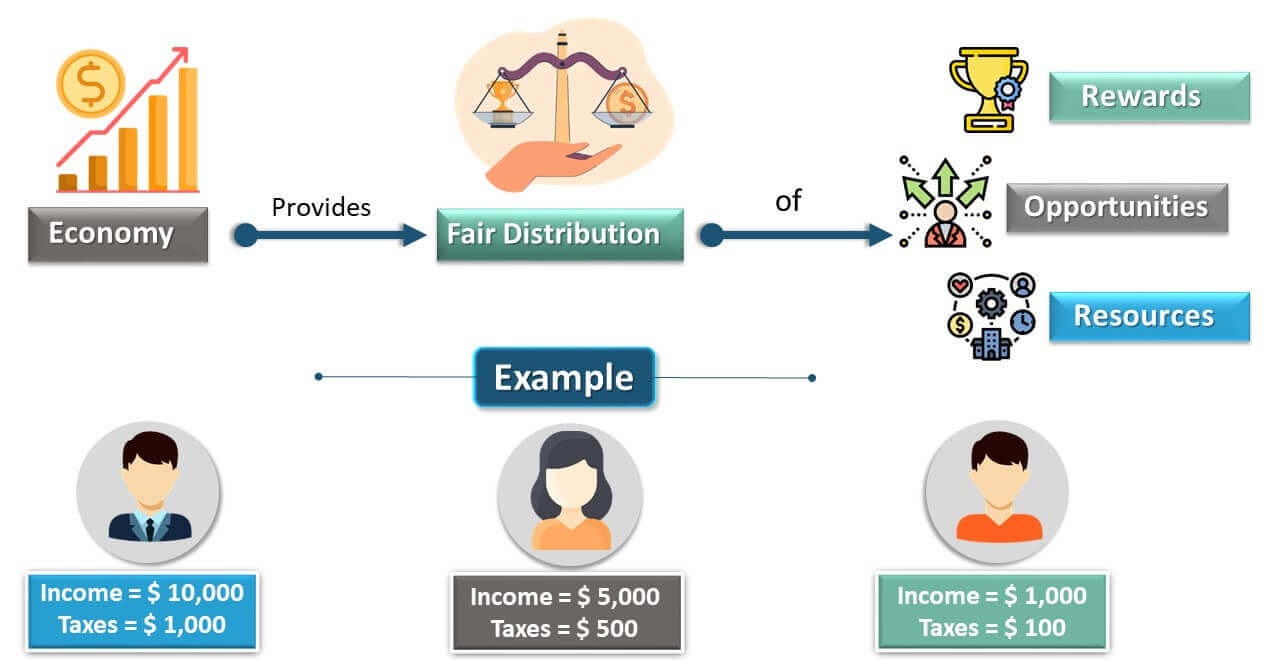

Equity

Equity refers to fairness in the distribution of income, wealth, and economic opportunities within a society.

- Includes horizontal equity (equal treatment of equals).

- Includes vertical equity (unequal treatment to reduce inequality).

- Measured using indicators like income distribution and poverty levels.

- Often conflicts with efficiency (trade-off).

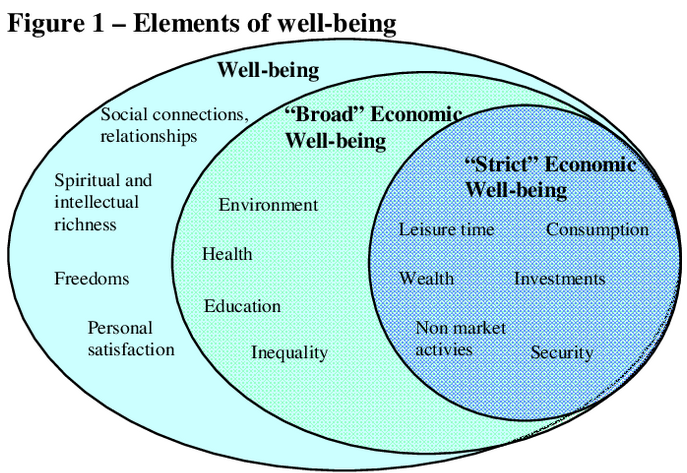

Economic Well-being

Economic well-being refers to the overall quality of life and standard of living of individuals in an economy.

- Includes material well-being (income, consumption).

- Includes non-material factors (health, education, environment).

- Measured using indicators like GDP per capita and HDI.

- May not always increase with economic growth.

Sustainability

Sustainability refers to meeting present needs without compromising the ability of future generations to meet their own needs.

- Involves environmental sustainability (resource conservation).

- Focuses on long-term economic growth.

- Addresses issues like climate change and resource depletion.

- Often requires government intervention.

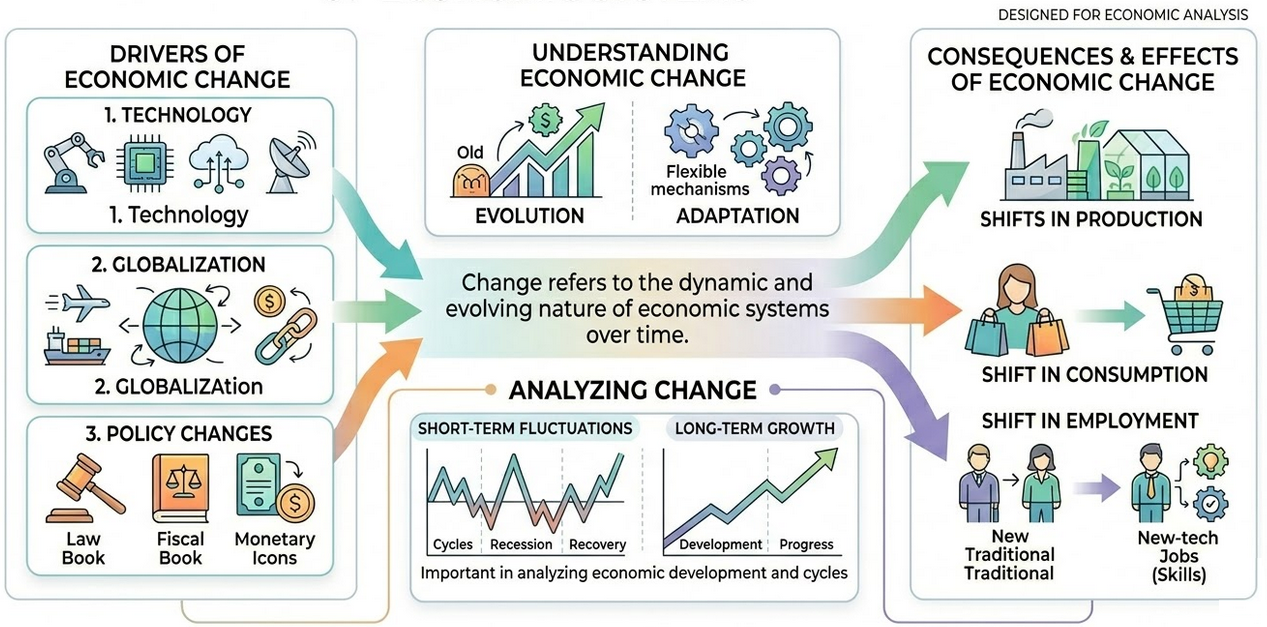

Change

Change refers to the dynamic and evolving nature of economic systems over time.

- Driven by technology, globalization, and policy changes.

- Leads to shifts in production, consumption, and employment.

- Includes both short-term fluctuations and long-term growth.

- Important in analysing economic development and cycles.

Interdependence

Interdependence refers to the mutual reliance between different economic agents and countries.

- Occurs through trade and specialization.

- Globalization increases interdependence between economies.

- Economic shocks can spread across countries.

- Key in international trade and global markets.

Intervention

Intervention refers to the involvement of governments in influencing economic outcomes.

- Includes tools like taxation, subsidies, and regulation.

- Used to correct market failures.

- Aims to improve equity and efficiency.

- May create unintended consequences (government failure).

Key Ideas:

- All nine concepts are interconnected and often appear together in exam questions.

- They form the basis for analysis and evaluation in DP Economics.

- Strong answers link multiple concepts rather than explaining them in isolation.

- Real-world examples should always connect back to these concepts.

Example 1

Explain how scarcity and choice lead to opportunity cost in an economy.

▶️ Answer / Explanation

Scarcity arises because resources are limited while wants are unlimited. This forces individuals and governments to make choices about how to allocate resources.

Whenever a choice is made, the next best alternative is sacrificed, which is known as opportunity cost.

For example, if a government allocates funds to healthcare instead of education, the opportunity cost is the benefits that would have been gained from investing in education.

This shows how scarcity leads to choice, and choice results in opportunity cost.

Example 2

Discuss the trade-off between efficiency and equity using an example.

▶️ Answer / Explanation

Efficiency focuses on maximizing output and using resources optimally, while equity focuses on fair distribution of income and resources.

For example, a government may impose higher taxes on high-income earners to redistribute income and improve equity.

However, higher taxes may reduce incentives to work and invest, leading to lower productivity and reduced efficiency.

This demonstrates a trade-off, where improving equity can come at the cost of efficiency, and policymakers must balance both objectives.

Overview (Short Summary) of the Nine Central Concepts:

| Concept | Description | Example |

|---|---|---|

| Scarcity | Limited resources relative to unlimited wants. | Limited supply of housing in cities. |

| Choice | Decisions made due to scarcity. | Choosing between spending or saving income. |

| Efficiency | Optimal use of resources to maximize output. | Producing goods at lowest cost. |

| Equity | Fair distribution of resources and income. | Progressive taxation. |

| Economic well-being | Quality of life and standard of living. | Access to healthcare and education. |

| Sustainability | Meeting present needs without harming future generations. | Using renewable energy. |

| Change | Dynamic nature of economies over time. | Technological advancements. |

| Interdependence | Economic agents rely on each other. | Global trade between countries. |

| Intervention | Government involvement in the economy. | Subsidies or taxes. |