Means of Answering the Economic Questions

Every economy must decide how to answer the three basic economic questions: what to produce, how to produce, and for whom to produce. These decisions are made through different mechanisms depending on the role of markets and government intervention.

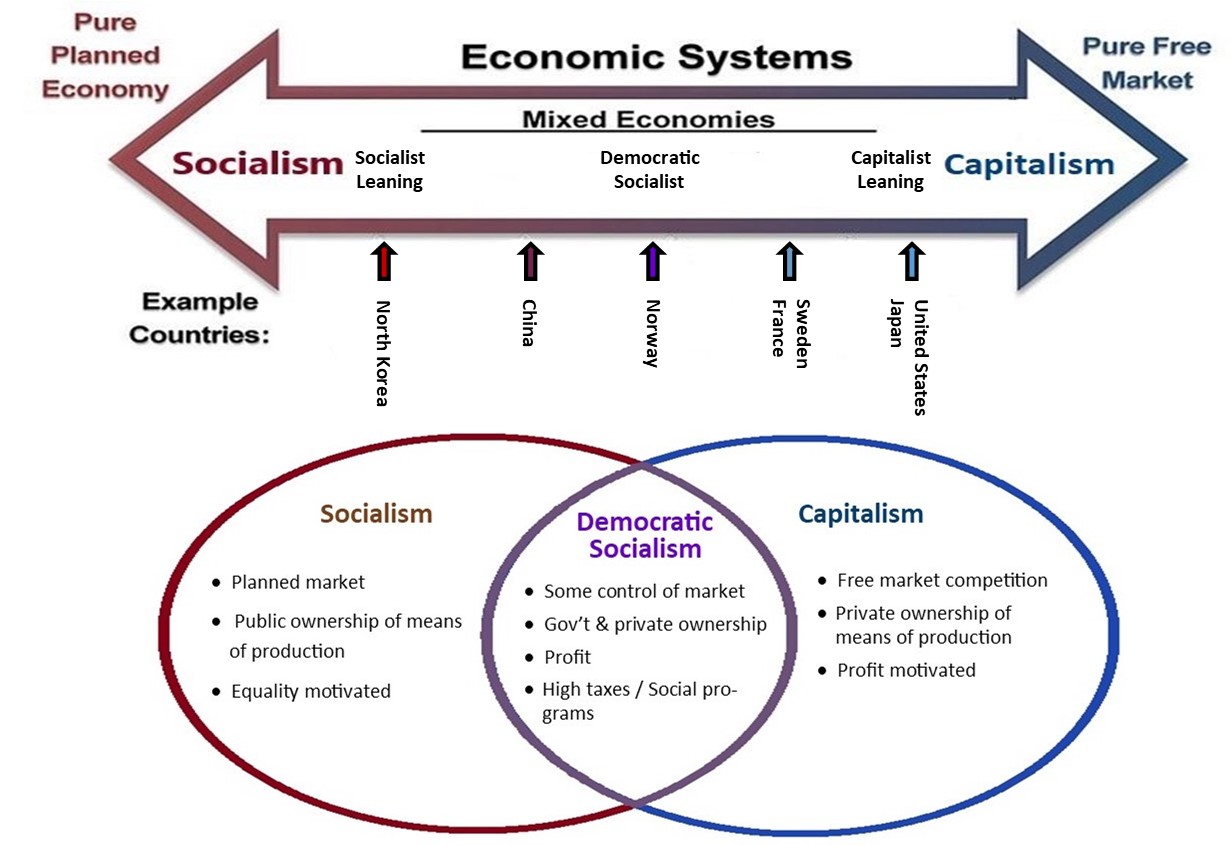

In general, economies lie on a spectrum between pure market systems and complete government control, with most real-world economies being a combination of both.

Economic Decisions = Market Forces + Government Intervention

Key Ideas:

- Markets use the price mechanism to allocate resources.

- Governments intervene to correct market failures and improve equity.

- Most economies operate as mixed systems.

- The balance between market and government affects efficiency and equity.

Market vs Government Intervention

The way economic questions are answered depends on whether decisions are made by market forces or by the government.

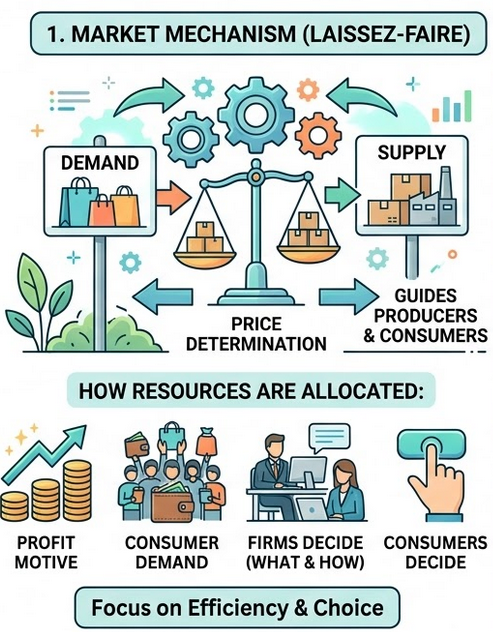

- Market mechanism — Prices are determined by demand and supply, guiding producers and consumers.

- Government intervention — The state influences decisions through policies such as taxes, subsidies, and regulations.

In markets:

| In government intervention:

|

Economic Systems

An economic system is the way a society organizes the production and distribution of goods and services. The three main types are:

- Free market economy

- Planned economy

- Mixed economy

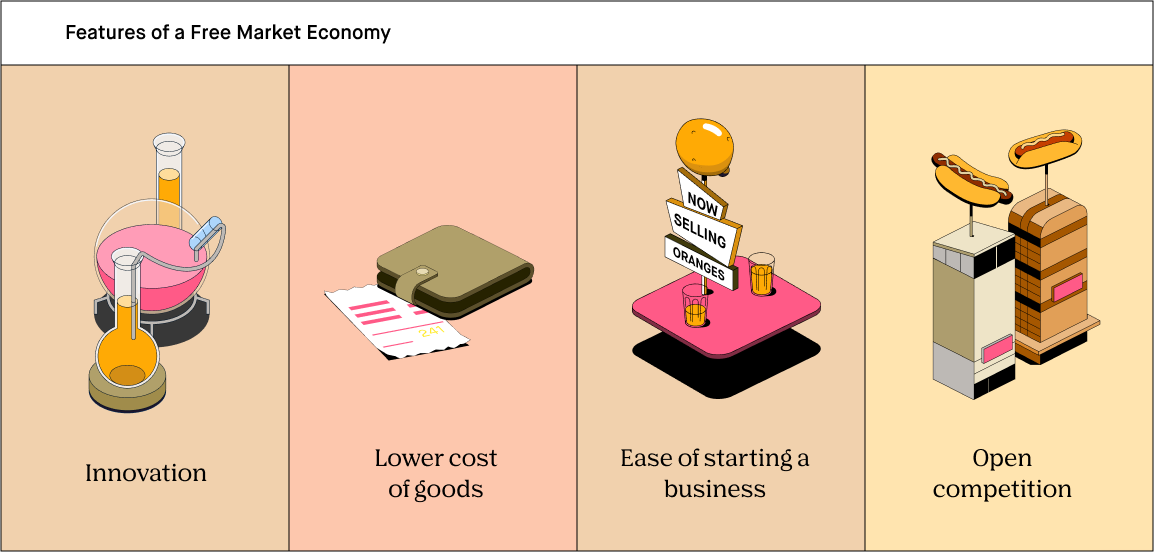

Free Market Economy

In a free market economy, economic decisions are made by individual consumers and firms through the price mechanism, with minimal government intervention.

- Prices are determined by demand and supply.

- Focus on efficiency and profit maximization.

- Limited role of government.

- May lead to income inequality and market failure.

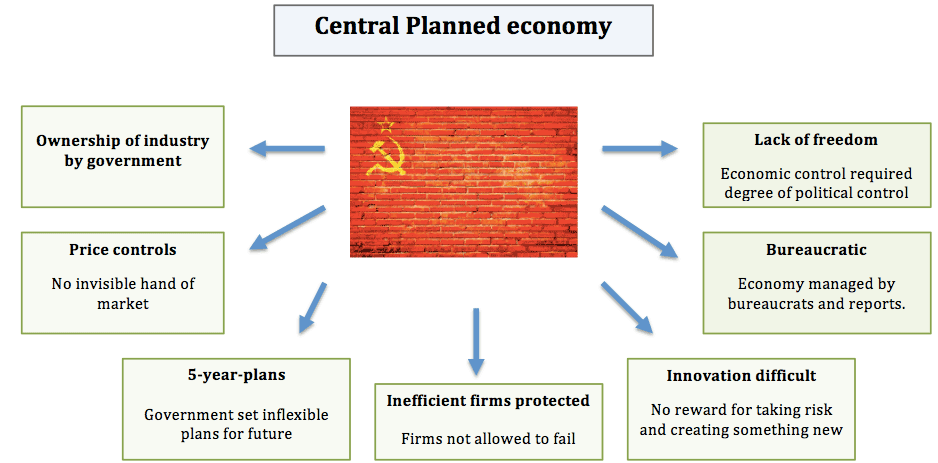

Planned Economy

In a planned economy, the government controls all major economic decisions regarding production and distribution.

- Resources are allocated by central planning.

- Focus on equity and social welfare.

- Prices may be set by the government.

- May lead to inefficiency and lack of incentives.

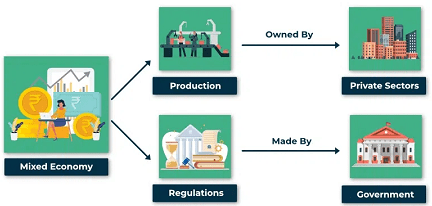

Mixed Economy

A mixed economy combines elements of both market and planned systems. Both private sector and government play important roles in decision-making.

- Markets allocate most resources.

- Government intervenes to correct market failures.

- Balances efficiency and equity.

- Most modern economies follow this system.

Comparison of Economic Systems:

| Aspect | Free Market Economy | Planned Economy | Mixed Economy |

|---|---|---|---|

| Decision Making | Consumers and firms | Government | Both market and government |

| Resource Allocation | Price mechanism | Central planning | Combination of both |

| Focus | Efficiency | Equity | Balance of both |

| Role of Government | Minimal | Extensive | Moderate |

Example 1

Explain how the price mechanism answers the basic economic questions in a free market economy.

▶️ Answer / Explanation

In a free market economy, the price mechanism determines resource allocation through demand and supply.

What to produce is decided by consumer demand — firms produce goods that are profitable.

How to produce is determined by firms choosing the most cost-efficient methods.

For whom to produce depends on consumers’ ability to pay, which is determined by income.

Thus, prices act as signals and incentives, guiding economic decisions without government control.

Example 2

Using an example, explain why most countries operate mixed economies.

▶️ Answer / Explanation

Most countries operate mixed economies because relying entirely on markets or government has disadvantages.

For example, markets may fail to provide public goods such as national defense or lead to income inequality.

Governments intervene by providing public services, regulating industries, and redistributing income.

At the same time, markets are allowed to function to ensure efficiency and innovation.

This combination allows economies to balance efficiency with equity.