Asymmetric Information

Asymmetric information occurs when one party in a transaction has more or better information than the other, leading to inefficient market outcomes.

Unequal information → Poor decisions → Market inefficiency

Explanation:

- Usually exists between buyers and sellers or insurers and consumers.

- The better-informed party can take advantage of the less-informed party.

- Leads to market failure and inefficient allocation of resources.

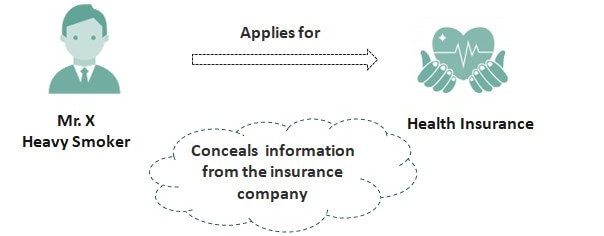

1. Adverse Selection

Adverse selection occurs when one party has more information before a transaction, leading to the selection of undesirable outcomes.

Explanation:

- The uninformed party cannot distinguish between high-quality and low-quality goods or customers.

- As a result, they may make decisions that attract higher-risk or lower-quality participants.

- This leads to inefficient market outcomes.

Why It Occurs:

- Hidden information before the transaction.

- Difficulty in verifying quality or risk.

- Lack of transparency.

Impact:

- High-quality products or low-risk individuals may leave the market.

- Market may become dominated by low-quality goods (“market for lemons”).

- Can lead to market breakdown.

2. Moral Hazard

Moral hazard occurs when one party changes behaviour after a transaction because they do not bear the full consequences of their actions.

Explanation:

- Occurs when individuals take greater risks because they are protected.

- The other party cannot fully observe or control their behaviour.

- Leads to inefficient outcomes.

Why It Occurs:

- Hidden actions after the transaction.

- Lack of monitoring or accountability.

- Protection from consequences (e.g. insurance).

Impact:

- Increased risk-taking behaviour.

- Higher costs for firms or insurers.

- Reduced efficiency in markets.

Key Differences:

| Aspect | Adverse Selection | Moral Hazard |

|---|---|---|

| Timing | Before transaction | After transaction |

| Problem | Hidden information | Hidden actions |

| Result | Wrong participants selected | Risky behaviour increases |

Economic Significance:

- Both lead to market failure.

- Reduce efficiency and welfare.

- May require government intervention or regulation.

Key Ideas:

- Asymmetric information leads to inefficiency.

- Adverse selection occurs before transactions.

- Moral hazard occurs after transactions.

- Important in insurance, finance, and labour markets.

Example 1

Explain adverse selection using the example of the used car market.

▶️ Answer / Explanation

Sellers know more about the quality of cars than buyers.

Buyers cannot distinguish between good and bad cars.

They offer an average price, causing sellers of high-quality cars to leave the market.

This results in a market dominated by low-quality cars.

Example 2

Evaluate how moral hazard can arise in the insurance market.

▶️ Answer / Explanation

Once individuals are insured, they may take greater risks.

For example, a person with car insurance may drive less carefully.

This increases the likelihood of claims.

Insurance companies face higher costs.

Thus, moral hazard leads to inefficiency in the market.