Main Forms of Government Intervention in Markets

1. Price Controls: Price Ceilings and Price Floors

Price controls are legal restrictions set by the government on prices to influence market outcomes.

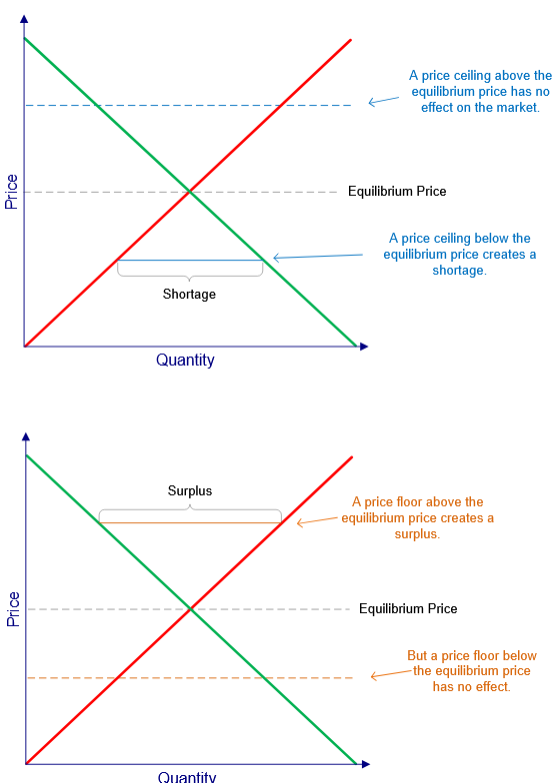

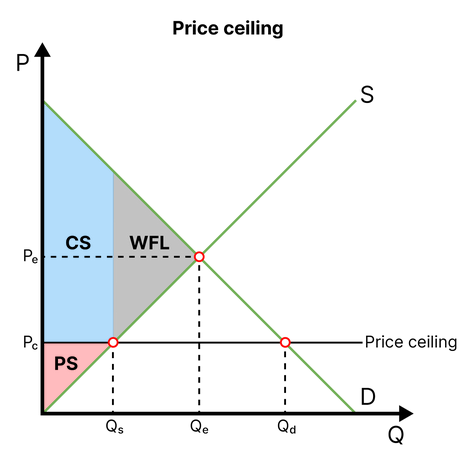

Price ceiling (maximum price):

Definition: A legally imposed maximum price that can be charged for a good or service.

- Usually set below equilibrium price.

- Aims to make goods more affordable for consumers.

- Leads to excess demand (shortage).

Effects price ceilings have on surplus:

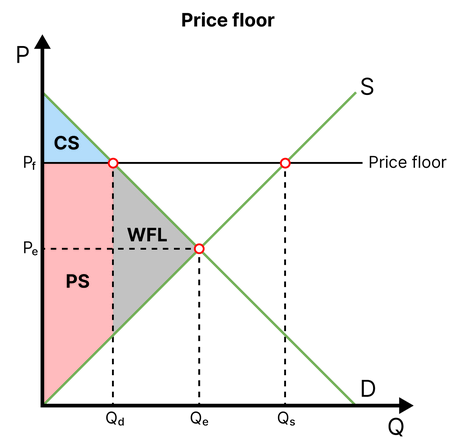

Price floor (minimum price):

Definition: A legally imposed minimum price that must be paid for a good or service.

- Usually set above equilibrium price.

- Aims to protect producers’ income.

- Leads to excess supply (surplus).

Effects price floors have on surplus:

Calculation (HL ONLY): Effects price ceilings/floors have on surplus:

Calculate the areas of the triangles after the ceiling/floor $\mathrm{(\frac{1}{2}×Base×Height)}$ and compare with the areas before the ceiling/floor.

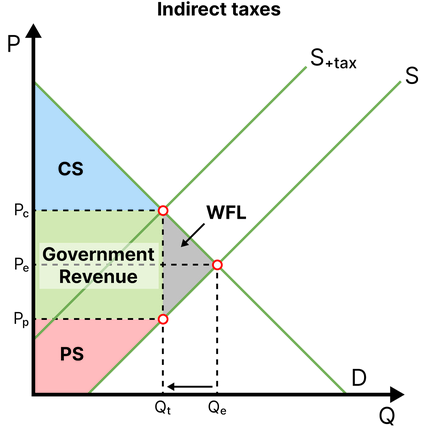

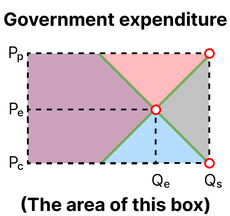

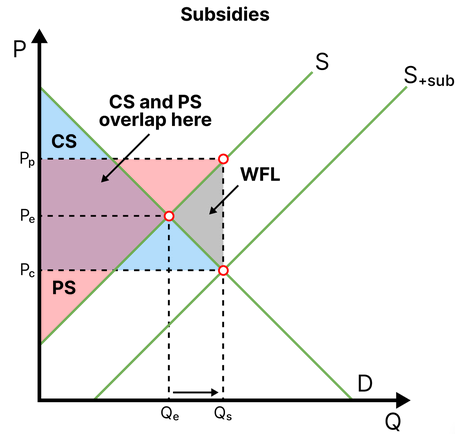

2. Indirect Taxes and Subsidies

Governments use taxes and subsidies to influence market outcomes.

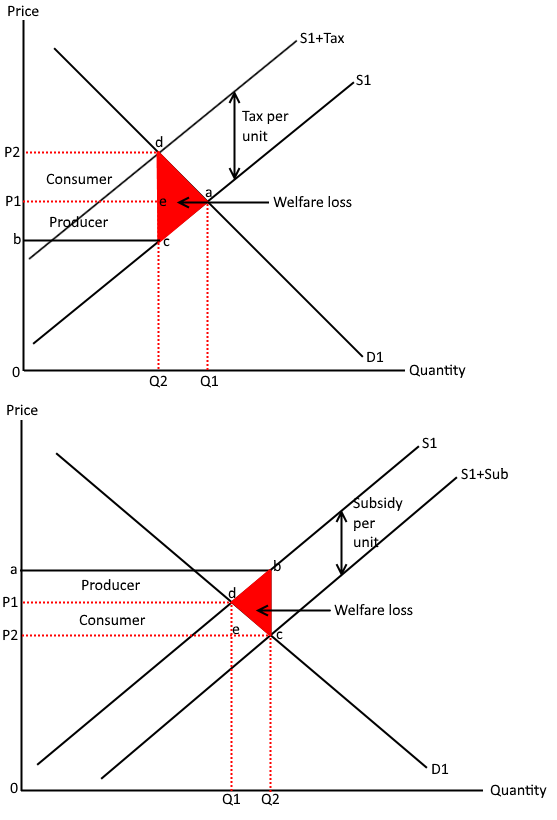

Indirect tax:

Definition: A tax imposed on goods and services rather than on income (e.g. VAT).

- Increases the cost of production for firms.

- Shifts the supply curve left.

- Leads to higher prices and lower quantity traded.

Effects indirect taxes have on surplus:

Subsidy:

Definition: A payment from the government to producers to reduce production costs.

- Lowers the cost of production.

- Shifts the supply curve right.

- Leads to lower prices and higher quantity traded.

Effects indirect taxes have on surplus:

Calculation (HL ONLY): Effects indirect taxes/subsidies have on surplus:

- Calculate the areas of the triangles after the tax/subsidy $\mathrm{(\frac{1}{2}×Base×Height)}$ and compare with the areas before the tax/subsidy.

- For subsidies, remember that since the PS and CS overlap in a certain area, that area is effectively counted twice when finding the social/community surplus.

Example 1

Explain why a price ceiling leads to a shortage.

▶️ Answer / Explanation

A price ceiling is a maximum price set below equilibrium.

At this lower price, quantity demanded increases while quantity supplied decreases.

This creates excess demand.

Thus, a shortage occurs.

Example 2

Evaluate the effect of an indirect tax on a market.

▶️ Answer / Explanation

An indirect tax increases production costs.

Supply decreases and shifts left.

Price rises and quantity traded falls.

This reduces consumption but generates government revenue.

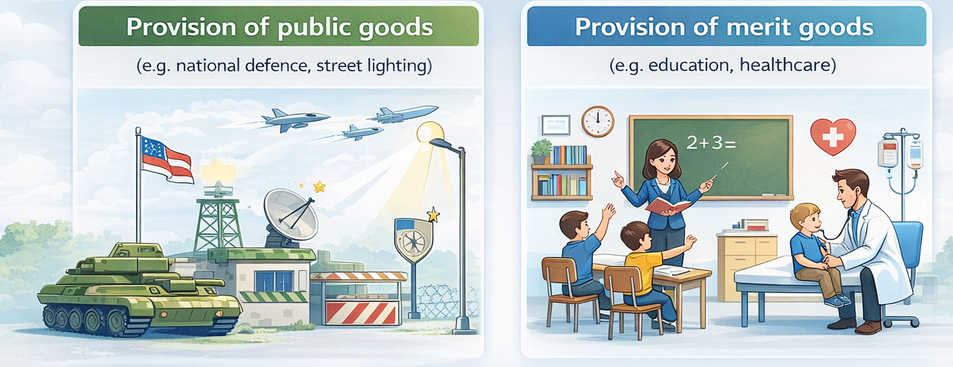

3. Direct Provision of Services

Governments may directly provide certain goods and services instead of leaving them to the market.

- Provision of public goods (e.g. national defence, street lighting).

- Provision of merit goods (e.g. education, healthcare).

- Services are often provided free or at subsidised prices.

Economic Explanation:

- Public goods are non-excludable and non-rival, so private firms may not supply them.

- Merit goods are often underconsumed in a free market.

- Government provision ensures adequate supply and improves social welfare.

Market underprovides → Government supplies

4. Command and Control Regulation and Legislation

Governments use laws and regulations to directly control economic activity.

- Laws to restrict or ban harmful activities (e.g. pollution limits, safety standards).

- Regulations to control production methods and quality.

- Penalties and fines for non-compliance.

Economic Explanation:

- Used to correct market failure, especially negative externalities.

- Ensures firms consider social costs of production.

- Directly influences behaviour without relying on price mechanisms.

Regulation → Controlled behaviour → Reduced harm

Evaluation Insight :

- Direct provision ensures access but may be costly and inefficient.

- Regulation is effective but may increase compliance costs for firms.

- Excessive intervention may lead to government failure.

Key Point:

- Direct provision addresses public goods and merit goods.

- Regulation controls harmful economic activities.

- Both aim to improve social welfare and efficiency.

- Governments use a mix of policies for effective intervention.

Example 1

Explain why governments provide public goods directly.

▶️ Answer / Explanation

Public goods are non-excludable and non-rival.

Private firms cannot charge consumers effectively.

This leads to underprovision in a free market.

Thus, governments provide them to ensure availability.

Example 2

Evaluate how regulation helps reduce negative externalities.

▶️ Answer / Explanation

Regulations set limits on harmful activities such as pollution.

Firms must follow rules or face penalties.

This reduces harmful output and improves social welfare.

However, strict regulations may increase costs for firms.

Example (HL- Only)

Equilibrium price = \( \mathrm{\$10} \), equilibrium quantity = \( \mathrm{100} \).

A price ceiling is set at \( \mathrm{\$8} \).

At this price: \( \mathrm{Q_d = 120} \), \( \mathrm{Q_s = 80} \).

Calculate the shortage and explain stakeholder effects.

▶️ Answer / Explanation

Shortage:

\( \mathrm{Shortage = Q_d – Q_s = 120 – 80 = 40} \)

Stakeholders:

- Consumers: benefit from lower price but face shortages.

- Producers: lose revenue due to lower price and lower sales.

- Government: may need to intervene further.

Example (HL- Only)

A government imposes a tax of \( \mathrm{\$5} \) per unit.

Original equilibrium: \( \mathrm{P = \$20, Q = 100} \).

After tax: consumers pay \( \mathrm{\$23} \), producers receive \( \mathrm{\$18} \), quantity = \( \mathrm{80} \).

Calculate tax revenue and explain stakeholder effects.

▶️ Answer / Explanation

Tax revenue:

\( \mathrm{Revenue = Tax \times Quantity = 5 \times 80 = 400} \)

Stakeholders:

- Consumers: pay higher price.

- Producers: receive lower price.

- Government: gains revenue.

- Market: quantity falls, reducing welfare.