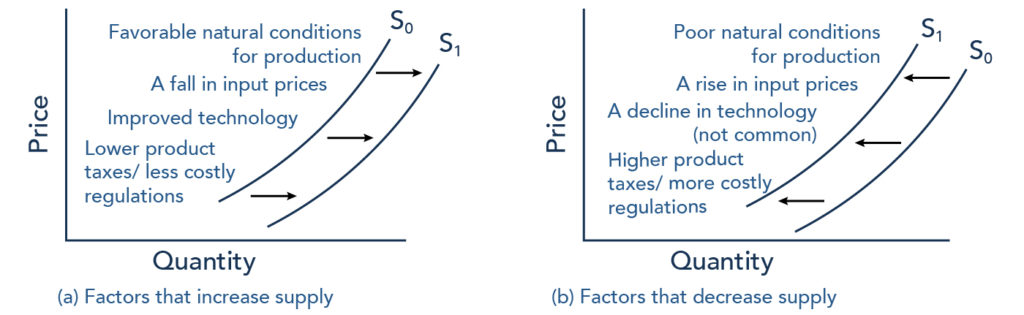

Non-Price Determinants of Supply

Changes in Costs of Factors of Production (FOPs)

The cost of factors of production such as land, labour, capital, and entrepreneurship directly affects a firm’s cost of production and therefore its willingness and ability to supply goods.

Cost of FOPs ↓ → Supply ↑

Cost of FOPs ↑ → Supply ↓

Explanation:

- If the cost of inputs (e.g. wages, raw materials) decreases, production becomes cheaper.

- Firms can supply more at every price level.

- This leads to a rightward shift of the supply curve.

- If the cost of inputs increases, production becomes more expensive.

- Firms reduce supply as profitability falls.

- This leads to a leftward shift of the supply curve.

Types of Factor Costs:

- Labour costs (wages, salaries)

- Raw material costs (oil, metals, agricultural inputs)

- Capital costs (machinery, interest rates)

- Rent for land or buildings

Any change in these costs affects overall production costs and supply decisions.

Example

Explain how a fall in wages affects the supply of a good.

▶️ Answer / Explanation

A fall in wages reduces the cost of labour, which is a factor of production.

This lowers the overall cost of production for firms.

As a result, firms can supply more at every price level.

This leads to a rightward shift of the supply curve.

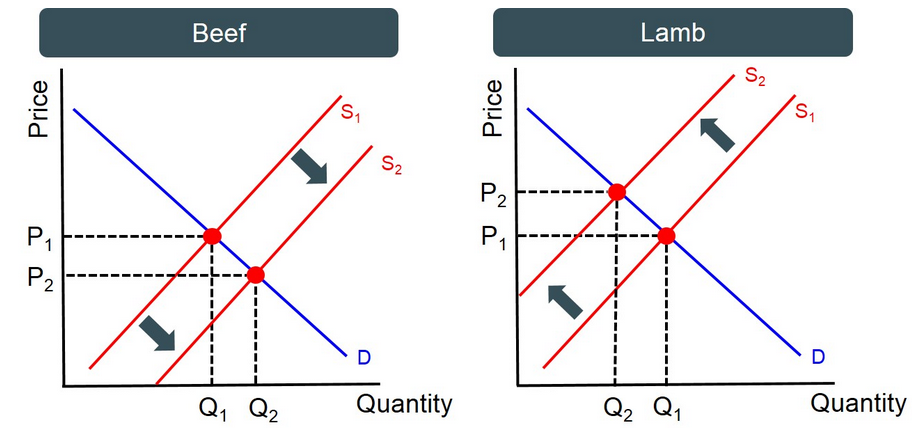

Prices of Related Goods (Joint Supply and Competitive Supply)

The supply of a good can be affected by the prices of related goods. These relationships arise when goods are either produced together (joint supply) or compete for the same resources (competitive supply).

Joint Supply

Joint supply occurs when two or more goods are produced together as a result of the same production process.

Examples include:

- Beef and leather

- Crude oil and petrol

- If the price of one product increases, producers increase production.

- This automatically increases the supply of the related joint product.

Explanation:

- Firms cannot easily produce one good without producing the other.

- Higher profitability of one product increases output of both goods.

- This leads to a rightward shift in supply of the related good.

Price of joint good ↑ → Supply of related good ↑

Competitive Supply

Competitive supply occurs when goods are produced using the same resources, so producing more of one means producing less of another.

Examples include:

- Farmers choosing between wheat and corn

- Factories producing cars or trucks

- If the price of one good increases, producers allocate more resources to it.

- This reduces the supply of the alternative (competing) good.

Explanation:

- Resources such as land, labour, and capital are limited.

- Firms shift resources to more profitable goods.

- This causes a leftward shift in supply of the competing good.

Price of competing good ↑ → Supply of this good ↓

Key Differences:

| Aspect | Joint Supply | Competitive Supply |

|---|---|---|

| Relationship | Goods produced together | Goods compete for resources |

| Effect of price increase | Supply of related good increases | Supply of other good decreases |

| Example | Beef and leather | Wheat and corn |

Example

Explain how an increase in the price of beef affects the supply of leather.

▶️ Answer / Explanation

Beef and leather are jointly supplied products.

If the price of beef increases, producers increase cattle production.

This results in more hides being available, increasing the supply of leather.

Thus, the supply of leather increases due to joint supply.

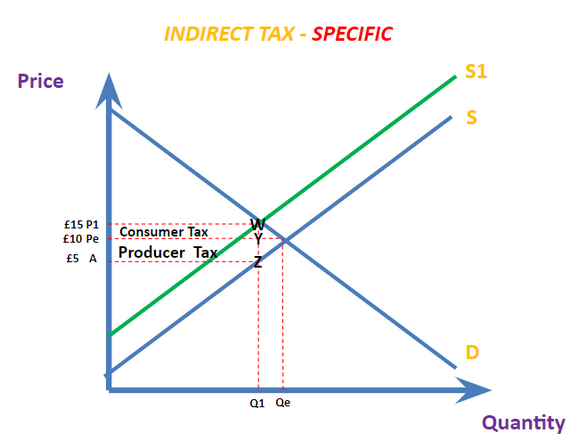

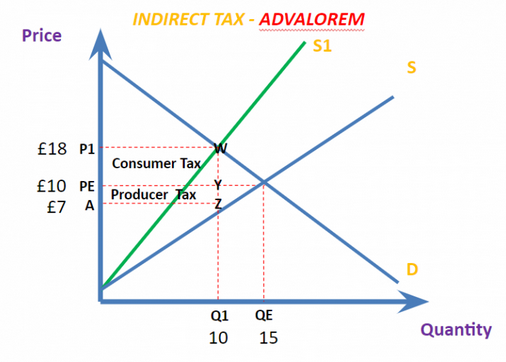

Indirect Taxes and Subsidies

Indirect taxes and subsidies are government interventions that directly affect firms’ costs of production, and therefore influence the quantity supplied at every price level.

Indirect Taxes

Indirect taxes are taxes imposed on the production or sale of goods and services (e.g. VAT, excise duties).

- Increase the cost of production for firms.

- Reduce profitability at each price level.

- Firms supply less at every price.

- Cause a leftward shift of the supply curve.

Tax ↑ → Costs ↑ → Supply ↓

Explanation:

- Taxes act like an additional cost per unit of output.

- Firms need higher prices to maintain profit levels.

- If prices remain unchanged, firms reduce output.

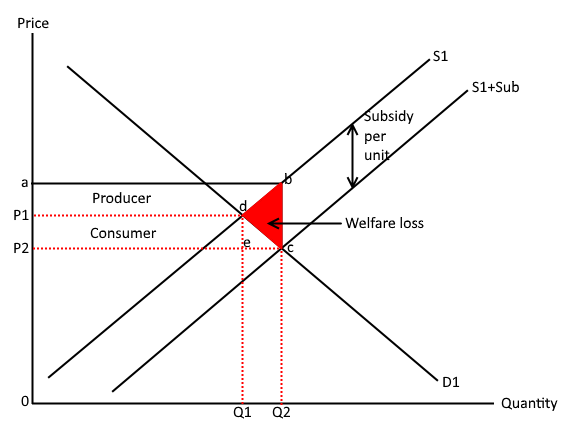

Subsidies

Subsidies are financial payments from the government to producers to encourage production.

- Reduce the cost of production.

- Increase profitability at each price level.

- Firms supply more at every price.

- Cause a rightward shift of the supply curve.

Subsidy ↑ → Costs ↓ → Supply ↑

Explanation:

- Subsidies effectively lower marginal cost.

- Firms are encouraged to increase production.

- Often used to promote industries such as agriculture or renewable energy.

Example

Explain how an increase in indirect taxes affects supply.

▶️ Answer / Explanation

An increase in indirect taxes raises production costs for firms.

This reduces profitability at each price level.

As a result, firms supply less output.

The supply curve shifts to the left.

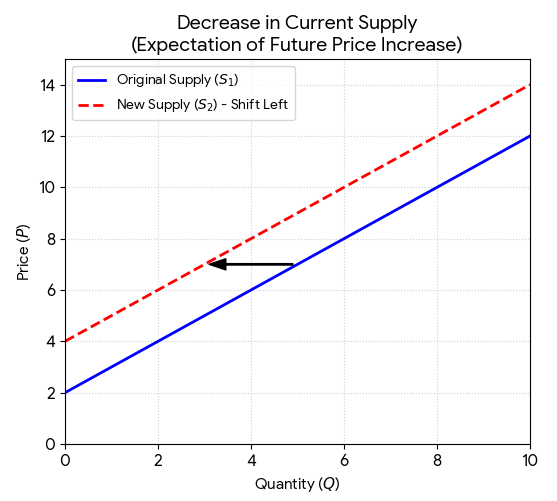

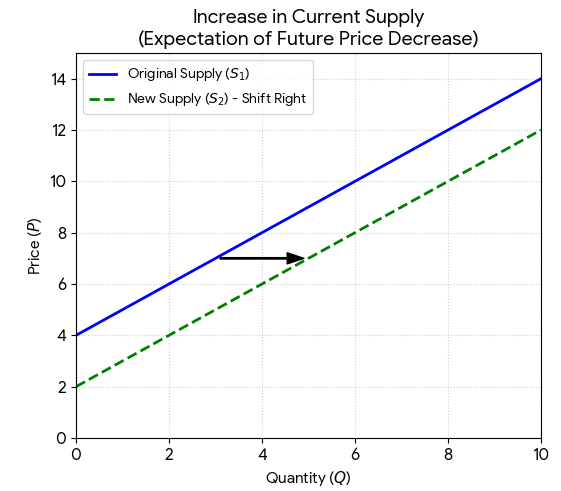

Future Price Expectations

Producers’ expectations about future prices can significantly influence the current supply of a good. Firms make decisions not only based on present conditions but also on anticipated future market trends.

Expected future price ↑ → Current supply ↓

Expected future price ↓ → Current supply ↑

Explanation:

- If producers expect prices to increase in the future, they may withhold supply now.

- This is because selling later could generate higher profits.

- As a result, current supply decreases, shifting the supply curve to the left.

- If producers expect prices to fall in the future, they will increase current supply.

- This allows them to sell before prices drop.

- As a result, current supply increases, shifting the supply curve to the right.

Conditions Where This Is Most Relevant:

- Storable goods (e.g. oil, grains, metals)

- Speculative markets

- Industries where firms can delay selling without major losses

For perishable goods, this effect is limited because goods cannot be stored.

Example

Explain how expectations of rising future prices affect current supply.

▶️ Answer / Explanation

If producers expect prices to rise in the future, they may reduce current supply.

This is because they prefer to sell later at a higher price to maximize profit.

As a result, current supply decreases and the supply curve shifts to the left.

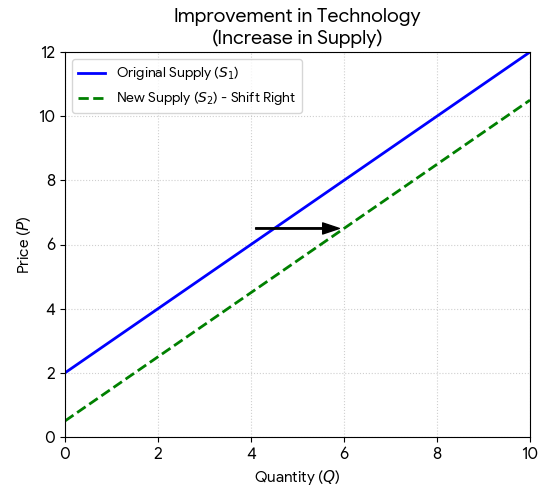

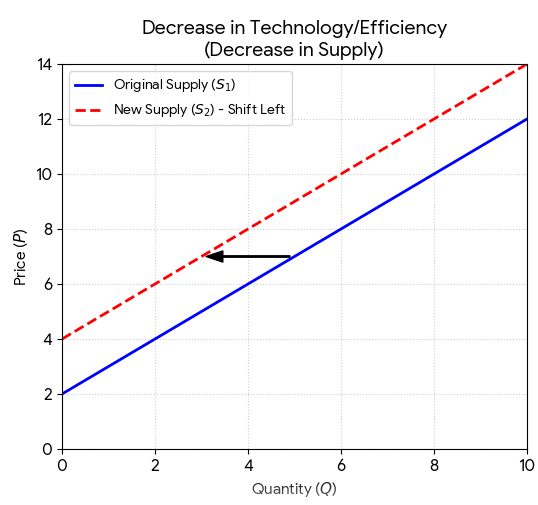

Changes in Technology

Technology refers to the methods and processes used in production. Changes in technology can significantly affect a firm’s efficiency and cost of production, and therefore influence supply.

Better technology → Costs ↓ → Supply ↑

Explanation:

- Improvements in technology make production more efficient.

- Firms can produce more output with the same inputs.

- This reduces average and marginal costs.

- As a result, firms are willing to supply more at every price level.

- This causes a rightward shift of the supply curve.

Conversely:

- If technology becomes outdated or less efficient, production costs may rise.

- This reduces supply and shifts the supply curve to the left.

Types of Technological Improvements:

- Automation (machines replacing labour)

- Improved production techniques

- Better logistics and supply chain systems

- Digitalization and data-driven production

Example

Explain how technological improvements affect the supply of goods.

▶️ Answer / Explanation

Technological improvements increase production efficiency.

This reduces the cost of producing each unit.

Firms can now supply more at every price level.

As a result, the supply curve shifts to the right.

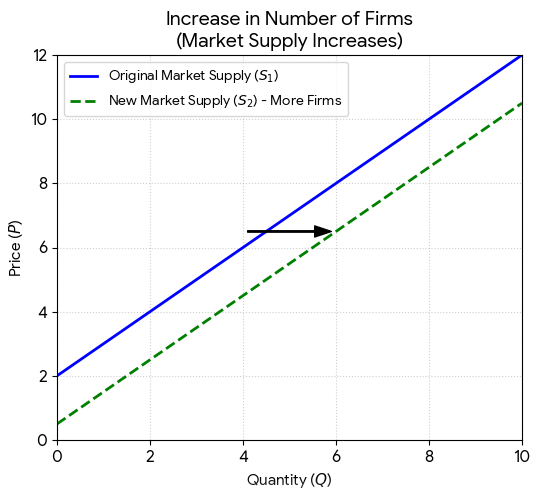

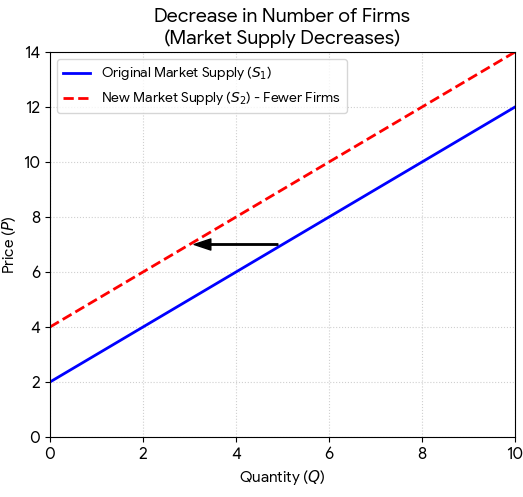

Number of Firms

The number of firms in a market directly affects total (market) supply. Since market supply is the sum of all individual firm supplies, any change in the number of producers will shift the supply curve.

More firms → Supply ↑

Fewer firms → Supply ↓

Explanation:

- If new firms enter the market, total production increases.

- Each firm contributes additional output, increasing market supply.

- This causes a rightward shift of the supply curve.

- If firms exit the market, total production decreases.

- Fewer firms means less output is supplied.

- This causes a leftward shift of the supply curve.

Reasons for Entry and Exit of Firms:

- Profitability — High profits attract new firms; losses drive firms out.

- Barriers to entry — High costs or regulations may prevent entry.

- Government policies — Taxes, subsidies, and regulations influence firm participation.

- Market conditions — Demand growth can encourage entry.

Example

Explain how the entry of new firms affects market supply.

▶️ Answer / Explanation

When new firms enter the market, they begin producing goods.

This increases total output in the market.

As a result, supply increases at every price level.

The supply curve shifts to the right.