A transition matrix, also known as a state transition matrix or Markov matrix, is a square matrix used to represent the probabilities of transitioning between different states in a system. Each element in the matrix represents the probability of moving from one state (represented by a row) to another state (represented by a column).

A transition matrix represents the probabilities of moving between different states in a Markov system or stochastic process.

Rows = Next state (i.e. destination)

Columns = Current state (i.e. origin)

Entries = Probability of transitioning from the current state to the next

Each column must sum to 1 (since total probability of leaving a state is 1)

Key Features:

- All entries must be between 0 and 1.

- The matrix is often square: if there are \( n \) states, the matrix is \( n \times n \).

- Used to model systems evolving over discrete time steps.

- Common in population models, economics, genetics, and game theory.

Example Population Movement Between Two Cities From A: 80% stay, 20% move to B Find the Transition Matrix ▶️ Answer/ExplanationLet the states be:

Transition Matrix \( T \): \( T = \begin{pmatrix} 0.8 & 0.3 \\ 0.2 & 0.7 \end{pmatrix} \)

|

Powers of a Transition Matrix

To find the probability distribution after multiple steps, we raise the transition matrix to a power:

\( T^n \) gives the probabilities of transitioning between states after n time steps.

Why use powers?

- \( T^2 \): shows 2-step transition probabilities

- \( T^3 \): shows 3-step transitions, and so on

- Multiplying the matrix by an initial state vector gives the system’s state at the next step

Example Use the matrix from the previous example: Find the probability of being in each city after 2 steps. ▶️ Answer/ExplanationGiven Transition Matrix \( T \): \( T = \begin{pmatrix} 0.8 & 0.3 \\ 0.2 & 0.7 \end{pmatrix} \) Find \( T^2 \) to get the 2-step transition matrix: $ T^2 = T \cdot T = \begin{pmatrix} 0.8 & 0.3 \\ 0.2 & 0.7 \end{pmatrix} \cdot \begin{pmatrix} 0.8 & 0.3 \\ 0.2 & 0.7 \end{pmatrix} $ $ = \begin{pmatrix} (0.8)(0.8)+(0.3)(0.2) & (0.8)(0.3)+(0.3)(0.7) \\ (0.2)(0.8)+(0.7)(0.2) & (0.2)(0.3)+(0.7)(0.7) \end{pmatrix} $ $ = \begin{pmatrix} 0.70 & 0.45 \\ 0.30 & 0.55 \end{pmatrix} $

|

Transition Diagrams in Discrete Dynamical Systems

Definition: A transition diagram is a directed graph that visually represents the movement between states in a system. It is commonly used with transition matrices in discrete dynamical systems.

Key Features:

- Nodes: Represent the different states in the system.

- Arrows: Show the direction of transition from one state to another.

- Weights on arrows: Indicate the probability or proportion of moving from one state to the next.

- Used with: Transition matrices \( T \), where entries \( T_{ij} \) represent the probability of moving from state \( j \) to state \( i \).

Connection to Transition Matrices:

Each column in the transition matrix corresponds to a state you are moving from, and each row shows the state you are moving to.

Use in Dynamical Systems:

If the initial state is given by a column vector (e.g. \( \begin{pmatrix} 100 \\ 0 \end{pmatrix} \)), then repeated multiplication by the transition matrix will simulate how populations evolve over time:

$ \text{Next state} = T \times \text{Current state} $ $ \text{After } n \text{ steps: } \quad \mathbf{x}_n = T^n \cdot \mathbf{x}_0 $

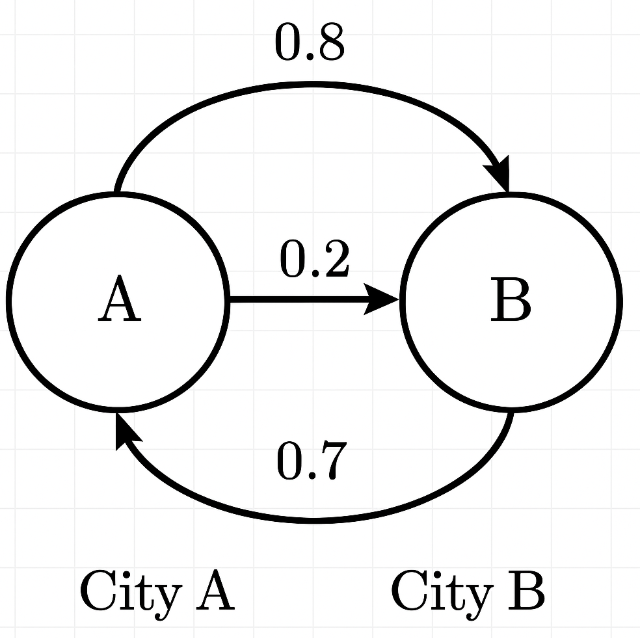

Example: Consider two cities, A and B:

Find Transition Matrix and describe Transition Diagram: ▶️ Answer/ExplanationSolution: Transition Matrix: $T = \begin{pmatrix} 0.8 & 0.3 \\ 0.2 & 0.7 \end{pmatrix} $ Transition Diagram:

|

A Markov Chain is a model for a system that transitions between states with fixed probabilities.

Key Property – Memorylessness:

The probability of moving to the next state depends only on the current state, not on the sequence of previous states.

Terminology:

States: The different conditions a system can be in

Transitions: Movements between states with associated probabilities

Transition Matrix: Encodes all transition probabilities