♦ Definition

Amortisation is the process of gradually paying off a debt with regular payments, where each payment is divided between the principal amount and the interest.

♦ The formula for the monthly payment \(P\) for an amortised loan of principal \(A\), with interest rate \(r\) and term \(n\) is:

\(P=\frac{rA}{1-(1+r)^{-n}}\)

♦ The total amount paid over the term of the loan is nP, and the total interest paid is

$nP − A$

♦ Formula for Monthly Payment \(P\)

\(P = \frac{rA}{1 – (1 + r)^{-n}}\)

Where:

\(A\) = Loan principal

\(r\) = Monthly interest rate (annual rate ÷ 12)

\(n\) = Total number of payments

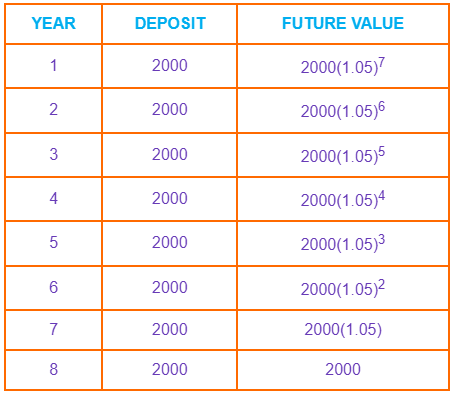

Example You invest $2000 at the end of each year, for 8 years, at a fixed interest rate of 5%. What will be the value at the end of the 8 years? Show each year values. ▶️Answer/ExplanationSolution: The $\$2000$ deposited each year earns interest for a different number of years:

So the total future value is: $FV = 2000(1.05)7 + 2000(1.05)6 + 2000(1.05)5 + … + 2000$ This is a geometric series where: First term \(u = 2000\), Common ratio \(r = 1.05\), Number of terms \(n = 8\). $S_n = u \cdot \frac{r^n – 1}{r – 1} = 2000 \cdot \frac{(1.05)^8 – 1}{0.05} \approx 2000 \cdot 9.549 = 19098.59 $ Final value of the annuity $≈ \$19098.59$ |

Example Loan: \$10,000 for 5 years at 6% annual interest. Total Paid: Total Interest: ▶️Answer/ExplanationSolution: \(P = \frac{(0.06/12) \times 10,000}{1 – (1 + 0.06/12)^{-60}} \approx \$193.33\) |