♦Definition

Simple Interest is the amount paid or earned only on the original principal over a certain time, not on accumulated interest. It is commonly used for short-term loans or investments, typically under one year.

♦Key Terminology

Principal (P): The original amount of money invested or borrowed.

Rate (r): The annual interest rate (expressed as a decimal).

Time (t): Time for which the money is invested or borrowed, in years.

Interest (I): The amount of money earned or paid as interest.

♦General Formula

$I = Prt$

Where:

$I$ = Interest

$P$ = Principal

$r$ = Annual simple interest rate (as a decimal)

$t$ = Time in years

♦Steps to Calculate Simple Interest

1. Convert percentage rate to a decimal:

e.g., $5\% = 0.05$

2. Multiply the decimal rate by the principal:

$P \times r$

3. Multiply by time:

$I = P \times r \times t$

Example A bank gives $3\%$ simple interest annually. Tom has £2000 in his account. How much interest does he earn in 1 year? ▶️Answer/ExplanationSolution: 1. $3\% = 0.03$ |

Example For Multiple years Borrowing £4800 for 3 years at $4\%$ simple interest per year. What will be the total interest. ▶️Answer/ExplanationSolution: 1. $4\% = 0.04$ |

♦Key Notes

- Simple Interest is not compounded.

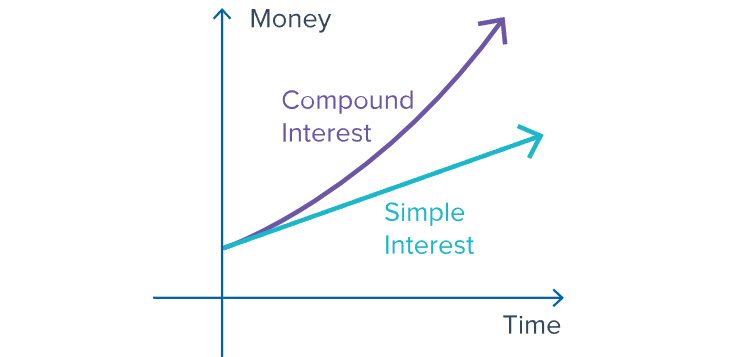

- Over time, simple interest will continue to grow by the same amount each year, while compound interest will grow faster and faster.

- It is calculated on the original principal only.

- If time is given in months, convert it to years: e.g., 6 months = 0.5 years

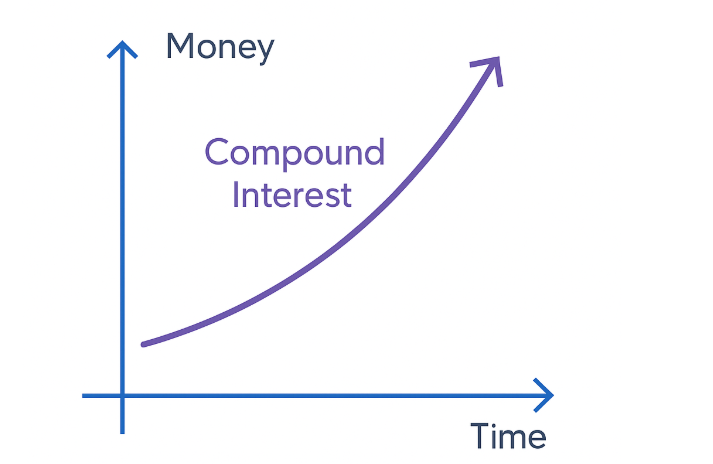

♦Compound Interest

Compound interest refers to the process where the interest earned on a principal amount is added back to the principal, and the new amount then earns interest. The formula for compound interest is:

\( FV = PV \left(1 + \frac{r}{100k}\right)^{kn} \)

Where:

\(FV\) is the future value after \(n\) years.

\(PV\) is the present value or principal amount.

\(r\) is the nominal annual interest rate (as a percentage).

\(k\) is the number of compounding periods per year.

\(n\) is the number of years.

Example Suppose we invest \$1000 at an annual interest rate of 6% compounded monthly for 5 years. Using the compound interest formula, we can find the future value after 5 years. Using the formula \( FV = PV \left(1 + \frac{r}{100k}\right)^{kn} \) ▶️Answer/ExplanationSolution: \( FV = 1000 \left(1 + \frac{6}{100 \times 12}\right)^{12 \times 5} = 1000 \left(1 + \frac{0.06}{12}\right)^{60} \approx 1349.86 \) |

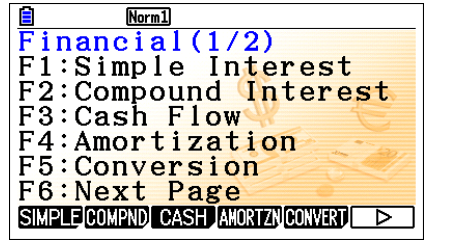

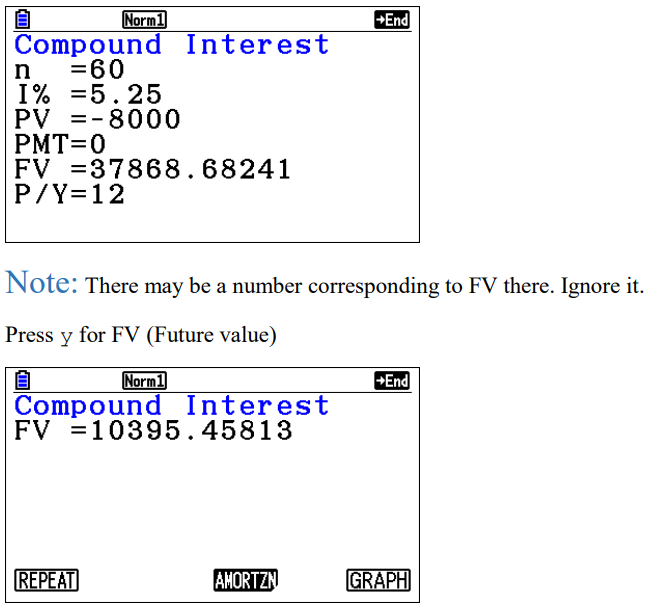

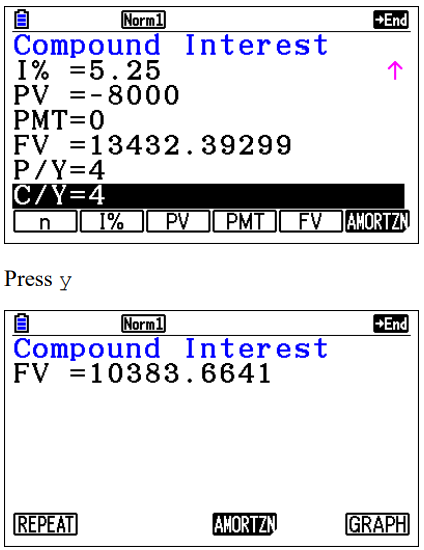

Example Andreas invests $8000$ euros in an account which pays a nominal annual interest rate of $5.25\%$, compounded monthly. Give all answers correct to two decimal places. Find (a)the value of the investment after 5 years; (b) the difference in the final value of the investment if the interest was compounded quarterly at the same nominal rate. ▶️Answer/ExplanationSolution: a. The value of the investment after 5 years is $A(t) = P\left(1 + \frac{i}{n}\right)^{nt} = 8000\left(1 + \frac{0.0525}{12}\right)^{12 \times 5} \approx 10395.46$ b. If the interest was compounded quarterly, then the amount would be $A(t) = P\left(1 + \frac{i}{n}\right)^{nt} = 8000\left(1 + \frac{0.0525}{4}\right)^{4 \times 5} \approx 10383.66$ Difference: $10395.46 – 10383.66$ = €11.80 Solution using GDC $\text{fx-CG50}$ (a) Go top, scroll to Financial app, l Press w and type the numbers in followed by leach time (remember that the

(b)

|